Defending Your Deal: Fire Insurance for Nevada Lake Tahoe Luxury Homes

Fire insurance is the elephant in the room for Lake Tahoe real estate, and in 2026, it became even more complicated.

High-intent buyers can find their dream home, negotiate a clean price, and enter escrow, only to hit a wall at the insurance stage.

If you are buying a luxury home on the Nevada side of Lake Tahoe, fire insurance needs to be part of your strategy before you make an offer.

Defending Your Deal Starts Before Escrow

Insurance is no longer something buyers can leave until the end of the transaction.

On the Nevada side of Lake Tahoe, wildfire risk, carrier guidelines, defensible space requirements, and policy exclusions can all affect whether a property is insurable on acceptable terms.

The good news: as of June 2026, Tahoe Tony’s clients have been able to secure fire coverage with the right local insurance professionals and the right strategy.

Calculate Your Nevada Tax Savings

Before weighing insurance complexity, see how Nevada’s no-state-income-tax structure may affect your overall financial picture.

Use the NV Tax Savings Calculator

1. What Changed in 2026

Nevada’s insurance market shifted significantly on January 1, 2026, when Assembly Bill 376 took effect.

Insurers can now legally remove wildfire coverage from a standard homeowners policy and sell it only as a separate, standalone product, or potentially not offer it at all.

That means buyers must confirm whether wildfire coverage is included in any policy quote or whether it must be sourced separately.

Nevada Has No FAIR Plan

Unlike California, Nevada does not currently have a state-run insurer of last resort.

If a carrier excludes wildfire and a buyer cannot secure standalone coverage, the property may be difficult or impossible to finance safely. This is why local insurance guidance is essential before contingencies are removed.

Planning a Nevada Move?

If your Tahoe purchase is part of a California-to-Nevada relocation strategy, start with the 2026 NV Residency Guide.

Explore the 2026 NV Residency Guide

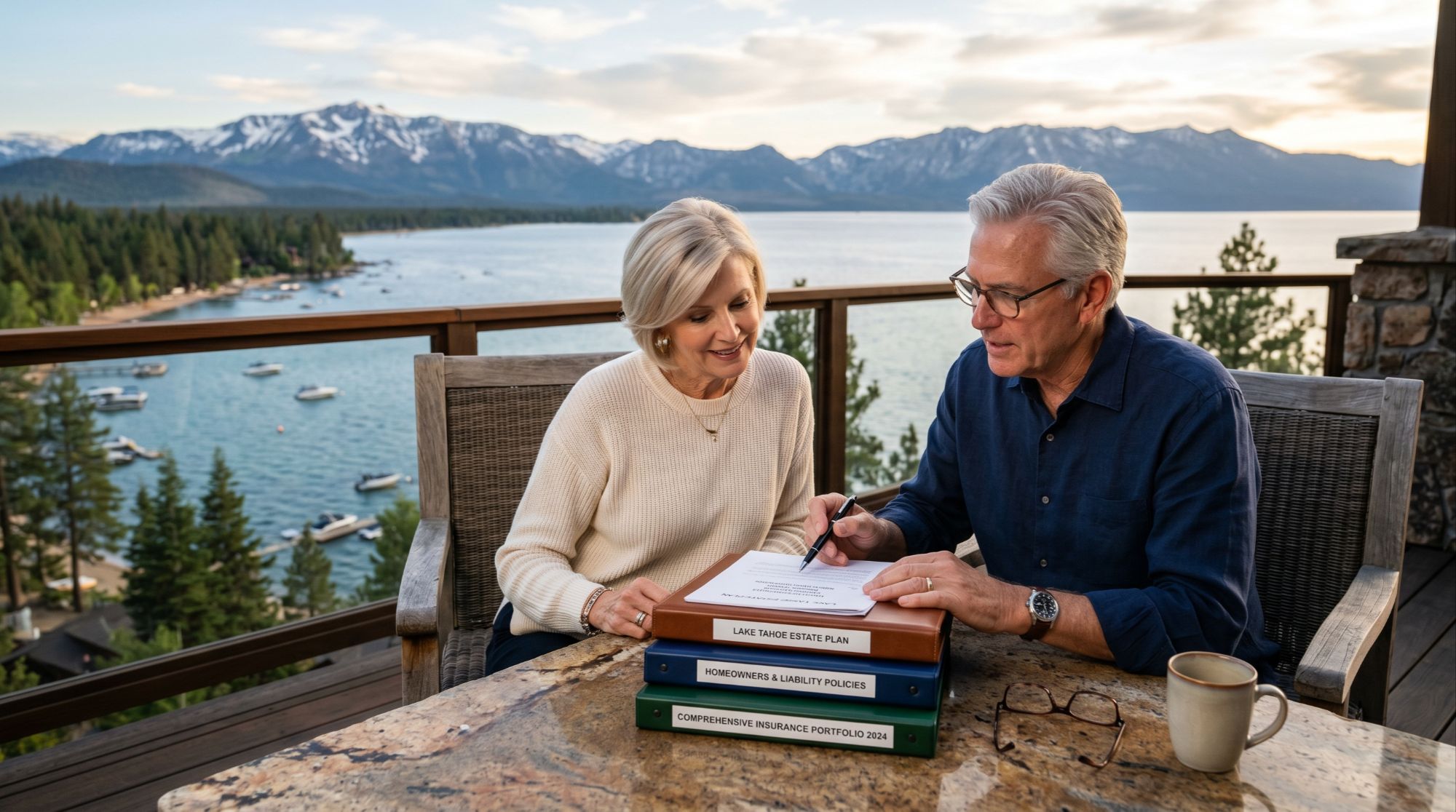

2. Plan for Three Layers of Coverage

Luxury buyers on the Nevada side of Lake Tahoe should think in layers, not just one homeowners policy.

Standard Homeowners Policy

This may cover theft, liability, water damage, and other standard risks, but wildfire coverage may no longer be included automatically.

Standalone Wildfire Policy

This is now the critical add-on. Surplus lines carriers and high-net-worth insurance specialists may remain active for qualified Tahoe Basin estates.

Earthquake Endorsement

Nevada sits in an active seismic zone, and standard homeowners policies typically exclude earthquake damage. This layer is easy to overlook but important for luxury buyers.

3. Defensible Space: Your First Step to Insurability

Before an insurer binds coverage, the property may need to pass a defensible space inspection.

On the Nevada side, inspections may involve Tahoe Douglas Fire Protection District for the South and East Shore, or North Lake Tahoe Fire Protection District for Incline Village and Crystal Bay.

The Three Defensible Space Zones

- Zone 0: 0 to 5 feet around the structure, with no combustible vegetation, mulch, or debris.

- Zone 1: 5 to 30 feet, often called the lean, clean, and green zone.

- Zone 2: 30 to 100+ feet, where fuel reduction and tree spacing help interrupt fire spread.

If a seller has not maintained vegetation or timber load, remediation can become a significant cost. This should be addressed early in the purchase contract, not discovered late in escrow.

Build a Defensible Nevada Residency Move

The Safe Harbor Checklist helps you think through the practical steps that support a cleaner, more strategic Nevada residency transition.

Download the Safe Harbor Checklist

4. Why Nevada Still Wins for High-Tax-State Buyers

Insurance is more complex than it used to be, but the Nevada side of Lake Tahoe remains one of the most compelling relocation markets for high earners.

Nevada has no state income tax. For a California resident earning $500,000 per year, the potential tax savings can be meaningful enough to absorb a more sophisticated insurance structure and still come out ahead.

Add a supply-constrained luxury market, year-round recreation, privacy, and a less restrictive tax environment, and the case for Nevada remains strong.

Final Thought

Fire insurance should not kill a strong deal, but it needs to be managed early and strategically.

The right approach is to evaluate wildfire coverage, defensible space, standalone policy options, earthquake exposure, and seller obligations before you remove contingencies.

With the right local team, Nevada Lake Tahoe luxury homes can still be insured, financed, and purchased with confidence.

Start an Insurance-Ready Property Search

Tahoe Tony can help connect you with specialized Nevada insurance professionals and identify properties with a stronger path to coverage.

Connect with Tahoe TonyThis post is for informational purposes only and does not constitute legal, tax, insurance, or financial advice. Consult licensed insurance, tax, legal, and financial professionals before making purchase or residency decisions.

Frequently Asked Questions

These are common questions luxury buyers ask about fire insurance, wildfire coverage, defensible space, and insurability on the Nevada side of Lake Tahoe.

Is fire insurance available for Nevada Lake Tahoe luxury homes?

Yes, fire insurance can still be available for Nevada Lake Tahoe luxury homes, but buyers need to start early. Wildfire risk, carrier requirements, defensible space, and policy exclusions can all affect whether a property is insurable on acceptable terms.

What changed with Nevada wildfire insurance in 2026?

Beginning in 2026, Nevada insurers may be able to separate wildfire coverage from a standard homeowners policy. That means buyers should confirm whether wildfire coverage is included or whether a standalone wildfire policy is needed.

Does Nevada have a FAIR Plan for fire insurance?

No. Unlike California, Nevada does not currently have a state-run FAIR Plan or insurer of last resort. This makes it especially important to secure insurance options before removing contingencies.

What insurance layers should Lake Tahoe luxury buyers consider?

Luxury buyers should typically evaluate a standard homeowners policy, standalone wildfire coverage, and an earthquake endorsement. Some buyers may also need high-net-worth policy structures or surplus lines coverage depending on the property.

What is defensible space, and why does it matter?

Defensible space is the managed area around a home designed to reduce wildfire risk. Insurers may look closely at vegetation, tree spacing, roof debris, mulch, and combustible materials near the structure before approving or binding coverage.

When should buyers start reviewing fire insurance options?

Buyers should review fire insurance options before writing an offer or as early as possible in escrow. Waiting until the end of the transaction can create financing problems, contingency issues, or unexpected costs.

Can Nevada tax savings offset higher insurance costs?

For some high-income buyers, Nevada’s no-state-income-tax structure may help offset the cost of a more sophisticated insurance plan. Buyers should evaluate the full picture, including taxes, insurance, property carrying costs, and residency planning.

Estimate potential savings here: NV Tax Savings Calculator.

Categories

Recent Posts

Managing Broker | License ID: BS.144620

+1(775) 815-8669 | tony.tuoto@exprealty.com